Difference between EPF and EPS and where does EPS money go when you change your job.

The Salaried individual are well aware of the part of their PF from employer's share goes to provide pension benefit for contributor. Let's discuss in details below.

Post last updated: June 4, 2024

Difference between EPF and EPS and where does EPS money go when you switch jobs.

The Salaried individual are well aware of the part of their PF from employer's share goes to provide pension benefit for contributor. Let's find the details below.

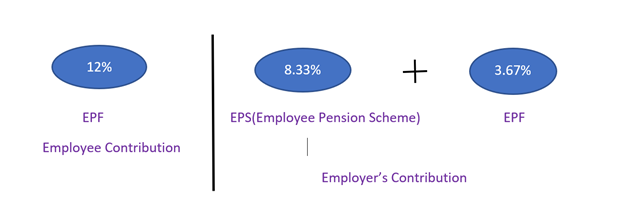

What are employee EPF contribution Components?

The EPF (Employee Provident Fund) contribution of an individual has 2 parts, one is employee contribution which is 12% (Basic Salary + DA), the other one is employer contribution which is also 12% (Basic Salary + DA) but part of it i.e. Basic Salary + DA) is contributed toward EPS (Employee Pension Scheme.) but 3.67% (Basic Salary + DA) is contributed toward the EPF but the max cap for EPS contribution is 1250/- if the 8.33% (Basic Salary + DA) >1250 rupees then maximum 1250 is deposited as the EPS contribution and the rest amount is deposited as part of EPF.

The Minimum amount to EPS which can be contributed to 541 Rupees (for (Basic Salary+ DA)>between 6500 and 15000) and Maximum amount after Oct 2014 can be 1250 Rupees (for (Basic Salary + DA)>15000).

The EPF and EPS are consolidated and are deposited to EFP and EPS contribution as can be seen on the EPF passbook as pension contribution.

When employee changes a new job then there is an option to either withdraw the PF or transfer the same to the next employer PF account. However, the UAN no. for the employee remains the same on the PF account no. with the new employer changes.

How to transfer PF on Job Change?

- To transfer the EPF from old employer to new employer there are two forms needed for the same Form 11 and Form 13, form 13 is the major form for it as form 11 only states the acknowledgement that you form a part of Employee Provident Fund.

When employee changes the job there is an evident option for transferring the EPF amount but what about the EPS amount accumulated, that amount is not even mentioned in the balance of transfer in the new EPF passbook of the employee. There are few options available for EPS too.

-

When PF is transferred the EPS, amount remains in the old account and is not transferred to new account.

-

The EPS amount can be withdrawn by the employee if he has not completed the job span of 10 year, both the EPS and EPF amounts can be withdrawn by the employee using the form 10C for EPS and Form 19 for EPF.

-

But if an employee has worked for more than 10 years and is a member of EPFO for more than 10 years, then he/she cannot withdraw the EPS amount but can opt for pensions like early pension starting from age of 50 or normal pension starting age of 58. However, the option for withdrawal of EPF is as usual always there with certain rules.

-

If an employee does not work after certain period and his EPS is accumulated with service more than 10 years or less than 10 years then he or she can apply for a certificate to be issued from EPFO which works as a proof of the service history and would be required if an employee rejoins a job or wants to start a pension for himself.

-

The form 10D can be used with EPFO certificate if any to set a pension, these forms have to be submitted in EPFO offices for verification and starting of employee pension.

The calculation of the EPS pension.

-

Max Average Salary (Basic Salary + DA) which can be considered for EPS is Rs.15,000, however employee may even have higher salary but max salary cap to consider is 15000 per month.

-

Max Pensionable Service which can be considered for EPS is 35 years

Formula for EPS pension is:

(Average Salary) X (Tenure of Service)/70

So, upon using the formula, (15000 * 35 / 70) = Rs. 7,500 per month is the maximum pension that employee can withdraw is 7500 max, the minimum pension which can be considered is 1000/-.

At last I would conclude with a suggestion that PF account holders should keep track of their PF Accounts both for EPF and EPS and should obtain the certificate for EPS account or withdraw the EPS if the tenure of 10 years is not completed with EPFO.

Have questions or need support? Feel free to reach out to us!

Email: admin@fincalci.com

Author: