Mastering Home Loan Management with Advance EMIs and Incremental EMI Strategy

Learn how to manage your home loan effectively with strategies like advance EMIs and incremental EMI increases. Save on interest and pay off your loan sooner.

Post last updated: December 25, 2024

Owning a home is a dream for many people, but the journey to owning a home often comes with a big responsibility—paying off the home loan. For many, the weight of monthly EMIs (Equated Monthly Installments) over a long period can feel overwhelming. But what if there was a way to lighten the load, save money, and shorten the time it takes to pay off your loan? Well, there is! By using strategies like advance EMIs and increasing your EMI each year, you can manage your loan more effectively and even save lakhs in interest.

One of the best ways to manage your home loan is by using tools like FinCalci’s Housing Loan Calculator. This tool helps you understand your loan structure, calculate EMIs, and plan your repayment strategies effectively. It gives you a clear picture of how paying extra or increasing your EMIs can impact your loan balance and help you become debt-free sooner.

The Challenge of Home Loans

Taking out a home loan is a big step. Whether you borrow ₹10 lakh or ₹1 crore, the financial commitment is significant. Home loans are typically spread over 10 to 30 years, and during the first few years, a large portion of your EMI goes toward paying the interest rather than the actual loan amount (principal). This makes it feel like you’re not making much progress, even though you’re faithfully paying your EMIs every month.

How Advance EMIs and Incremental EMIs Can Help

1. Advance EMIs: Advance EMI means paying more than your usual EMI. For example, imagine you decide to pay one extra EMI each year. This extra payment directly reduces your loan’s principal, lowering the outstanding balance on which interest is charged. The faster you reduce the principal, the less interest you’ll pay in the long run, and the sooner you’ll be free from the loan. It’s a simple yet powerful strategy to manage your loan better.

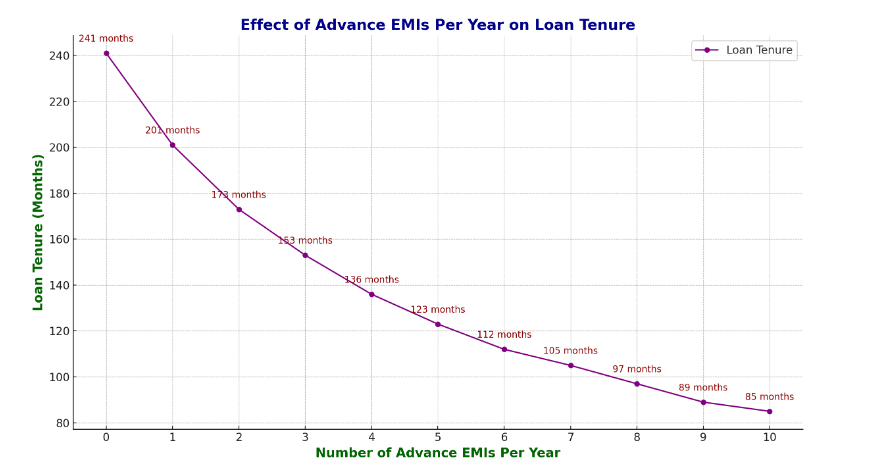

Below image shows the graph how paying only advance emi can have impact on home loan tenure. This is amazing, as it does not depend on how much amount you have taken as home loan.

2. Incremental EMIs: Incremental EMIs involve gradually increasing your EMI amount every year. As your salary increases over time, you can afford to pay more. Even small increases—say, 5% more each year—can make a big difference in how quickly you repay the loan. This strategy shortens your loan tenure and reduces the interest you end up paying.

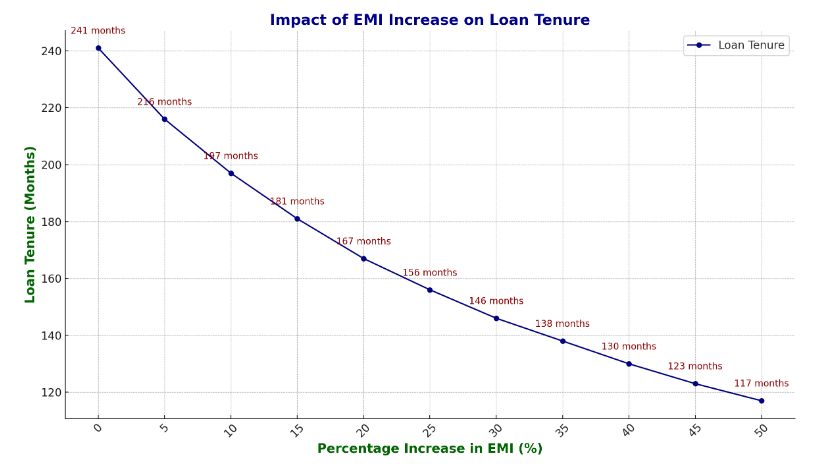

Below image shows the graph how only increasing emi % each year can have impact on home loan tenure. This is amazing, as it does not depend on how much amount you have taken as home loan.

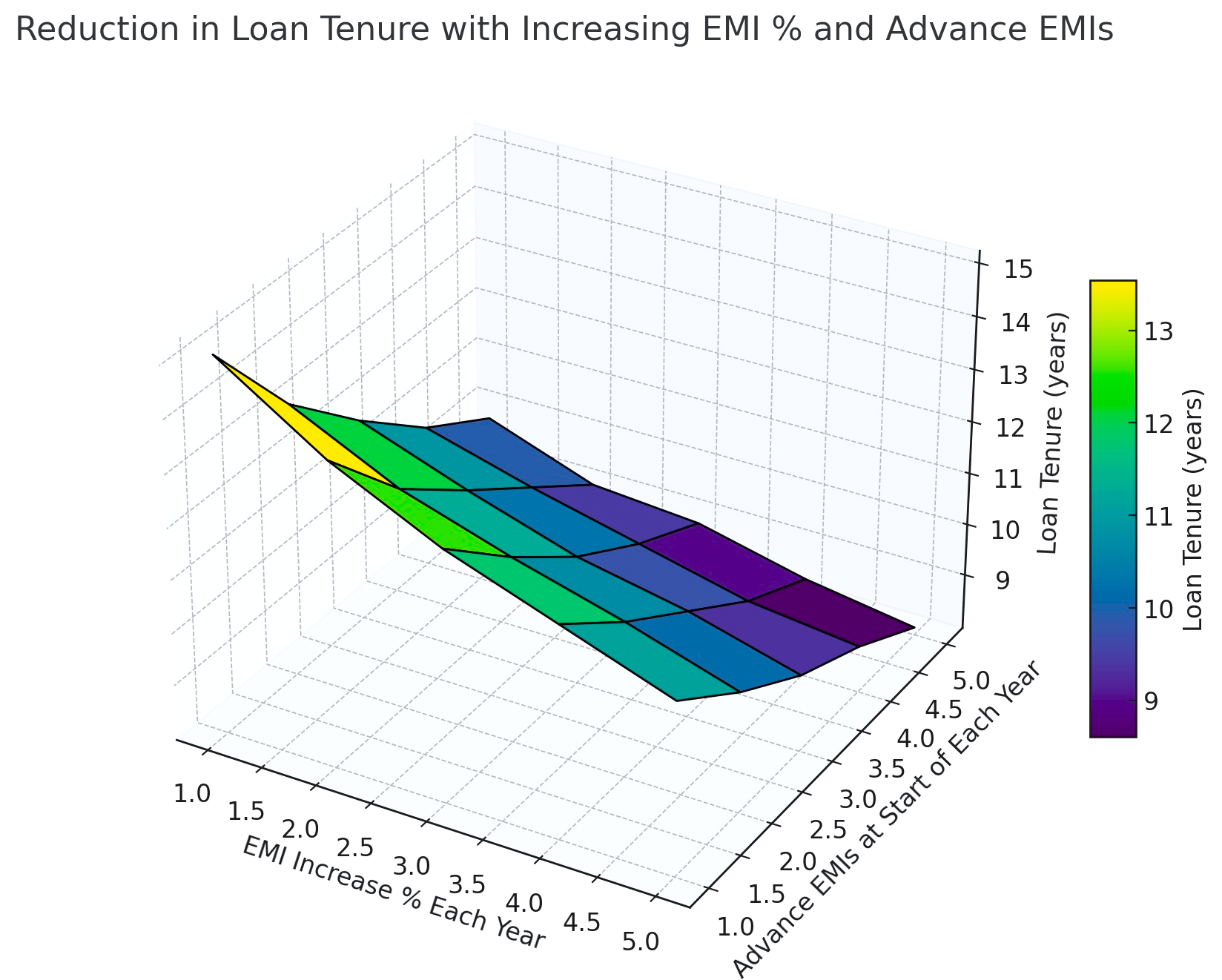

Below is the combined graph which show the glimpse how combining both the strategies mindfully can impact the home loan.

Real-Life Example

Let’s look at a real-life example to understand how these strategies work in practice. Suppose you’ve taken a home loan of ₹1 crore at 8% interest for 20 years. Your monthly EMI in this case would be ₹83,644. Here’s how applying the strategies could benefit you:

1. Advance EMI Payments: If you choose to pay one extra EMI of ₹83,644 each year, you can reduce your loan tenure to about 16.5 years. You’ll pay off the loan nearly 3.5 years earlier, and in the process, you’ll save ₹19.5 lakh in interest. That’s a lot of money that could go toward something else, like investments or personal savings!

2. Incremental EMIs: If you decide to increase your EMI by 5% every year, your loan tenure would shorten to about 14 years. You’d save ₹29 lakh in interest over the entire loan period. This means you’re not just paying off the loan faster, but also putting more money into your pocket by avoiding high interest.

3. Combining Both Strategies: Now, imagine combining both strategies: paying one extra EMI every year and increasing your EMI by 5% annually. In this case, your loan tenure would be reduced to around 12.5 years, and you’d save ₹37 lakh in interest! You’ll be free from debt much sooner and have saved a significant amount on interest.

Benefits of These Strategies

1. Pay Off Your Loan Faster: By using advance and incremental EMI strategies, you can shorten your loan tenure. This means you'll be free of debt years earlier than you’d originally planned, which can bring you peace of mind.

2. Save on Interest: The faster you pay off the principal, the less interest you pay. Since interest is calculated on the remaining balance of the loan, reducing the principal earlier helps you save a lot of money in the long run.

3. Improve Your Credit Score: Closing your loan faster can positively impact your credit score. A higher credit score can help you get better financial products in the future, like lower interest rates on personal loans or credit cards.

4. Build Financial Discipline: Committing to higher EMIs encourages you to be more disciplined with your finances. Over time, this habit can help you manage other aspects of your personal finances more effectively, like budgeting, saving, and investing.

Important Considerations

Before jumping into these strategies, it’s important to keep a few things in mind:

-

Prepayment Charges: Some banks charge fees for early repayments or extra payments toward your loan. Be sure to check your loan agreement and understand any charges that might apply.

-

Emergency Fund: While it’s great to pay off your loan early, don’t forget to keep an emergency fund. Life is unpredictable, and you’ll want to make sure you have enough savings for any unexpected situations like medical expenses or job loss.

-

Investment Returns: Sometimes, investing your extra money in a mutual fund or other investment options may give you better returns than paying off the loan early. Compare the savings from paying off the loan earlier with potential investment returns before making a decision.

Conclusion

Managing a home loan doesn’t have to feel like a never-ending burden. By using strategies like paying advance EMIs and increasing your EMI percentage each year, you can pay off your loan faster, reduce the interest you pay, and achieve financial freedom sooner. Tools like FinCalci’s Housing Loan Calculator can help you plan your repayments and see how much you can save by using these strategies. By taking small steps today, you can work toward being debt-free tomorrow and build a more secure financial future.

Housing Loan Calculator

Estimate your housing loan EMIs and repayment schedule

Calculate the EMI and the total repayment for your housing loan based on the loan amount, interest rate, tenure, advance EMIs and lumpsum payments

Thirty lakh

Seven only

Twenty only

If you want pay off your loan faster and save on interest? Adopt these simple strategies:

- Increase your EMI each year by some % to pay off your loan quicker

- Make Lump Sum Payments whenever you can.

- Pay Advance EMIs to cut down on interest

Monthly EMI

₹0

0

Total Loan Paid including Interest

₹0

0

Total Interest Paid

₹0

0

| EMI Number | EMI Amount | Towards Principal | Towards Interest | Lump Sum Paid | Advance EMI Paid | Outstanding Loan |

|---|

Have questions or need support? Feel free to reach out to us!

Email: admin@fincalci.com

Author: